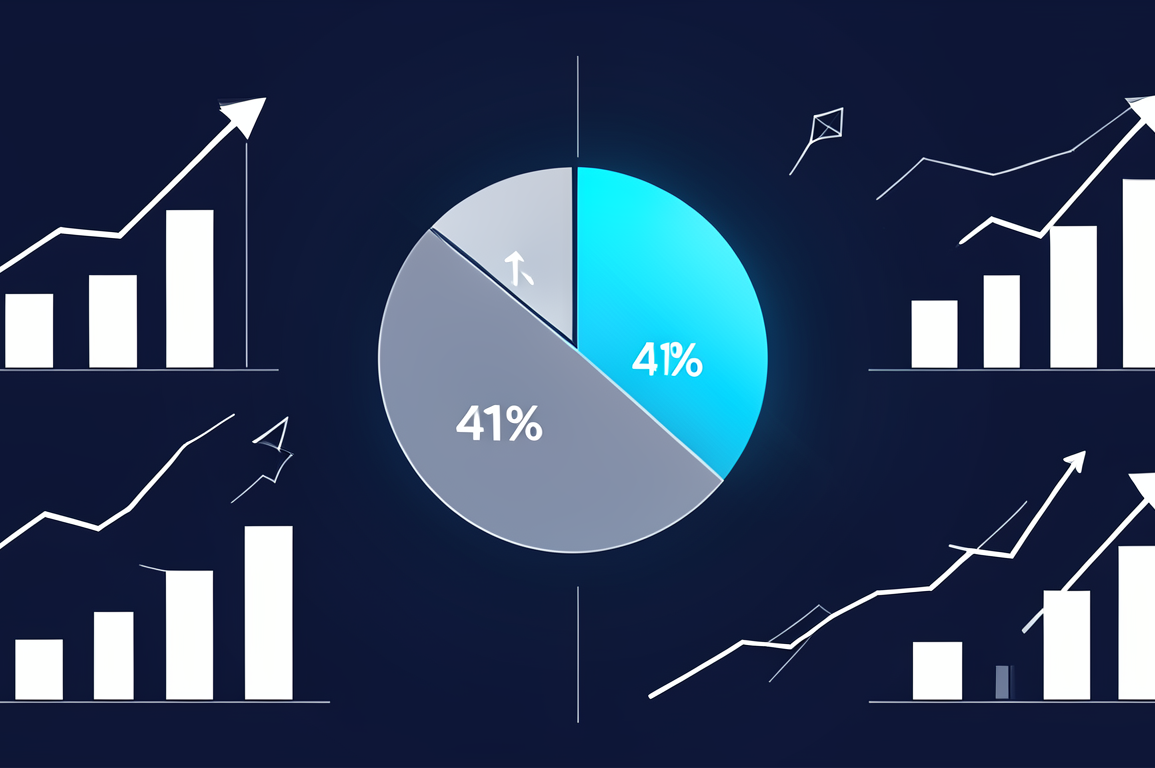

Artificial intelligence startups have captured 41% of venture capital deployed globally, securing approximately $52 billion of the $128 billion invested across all sectors, according to data reported by TechCrunch. The concentration represents the highest share directed to a single technology category in more than two decades of venture investing.

The allocation marks a fundamental reordering of venture priorities, with AI companies now receiving nearly double the share captured by software-as-a-service firms during their peak funding cycle in 2021. Traditional enterprise software, fintech, and consumer internet companies have seen their collective share compress to levels not witnessed since the mid-2010s.

The capital flow reflects both conviction and constraint. Limited partners—the institutional investors backing venture funds—have signalled clear preferences for AI exposure, whilst simultaneously reducing commitments to generalist funds lacking domain expertise. This dynamic has forced established firms to retrofit their investment theses whilst specialist AI-focused funds have raised capital at unprecedented velocity.

Returns data, whilst still early-stage, supports the reallocation. TechCrunch reports that AI-focused funds raised between 2020 and 2023 are tracking ahead of their vintage peers on paper markups, though realised returns remain limited given the sector’s relative youth. The performance has been sufficient to sustain momentum even as broader venture returns have disappointed following the 2021 peak.

Market Implications

The concentration creates distinct winners and losers across the venture ecosystem. Established firms with early AI positions—Andreessen Horowitz, Sequoia Capital, and Index Ventures among them—have strengthened their market position through portfolio appreciation and preferential access to subsequent rounds. Generalist funds without meaningful AI exposure face pressure on both fundraising and deal flow.

For founders outside the AI sector, the environment has become materially more challenging. Non-AI startups report elongated fundraising cycles and compressed valuations as investors redirect partner time and fund reserves toward artificial intelligence opportunities. Sectors previously considered venture-viable—including consumer applications, vertical SaaS, and B2B marketplaces—now struggle to command attention absent clear AI integration strategies.

The capital concentration also raises portfolio construction questions for venture firms. At 41% sectoral allocation, funds face correlated risk exposure that exceeds traditional diversification guidelines. A broad AI market correction would impact portfolio values across multiple positions simultaneously, potentially amplifying downside scenarios.

Historical Context

The current AI share exceeds previous sectoral peaks, including internet infrastructure in 1999 (approximately 35% of venture capital) and mobile applications in 2011 (roughly 28%). However, those earlier cycles featured broader technology platforms supporting diverse business models, whilst today’s AI concentration centres heavily on foundation model developers and immediate application layers.

The comparison suggests caution. Both previous cycles experienced sharp corrections when capital deployment outpaced revenue materialisation. The internet bubble collapsed when advertising and e-commerce revenues proved insufficient to support valuations, whilst mobile investing normalised as user acquisition costs exceeded unit economics for most applications.

AI companies face analogous questions around enterprise adoption rates, willingness to pay for model access versus open-source alternatives, and the timeline for productivity gains to translate into budget reallocation. Early revenue traction has been promising, but sustainability at current valuations requires sustained growth at unprecedented scale.

Forward Indicators

Several metrics will signal whether the current allocation proves durable. Enterprise AI spending growth, measured through cloud infrastructure consumption and model API usage, provides real-time demand validation. Customer retention rates for AI applications will indicate whether initial deployments expand or contract following pilot phases.

Venture fund formation data will reveal whether capital continues flowing toward AI-specialist managers or begins rotating back toward generalist strategies. Exit activity—particularly acquisitions by strategic buyers and public market receptivity to AI offerings—will determine whether paper returns convert to realised gains.

The 41% share represents investor conviction that artificial intelligence constitutes a fundamental platform shift rather than a feature enhancement. Whether that conviction translates to sustained returns depends on execution timelines that extend well beyond current funding cycles.