A widening chasm in artificial intelligence returns threatens to stratify the corporate landscape, with a small cohort of organisations capturing the vast majority of AI-generated value whilst their competitors struggle to realise meaningful benefits, according to PwC’s 2026 AI Performance Study released this week.

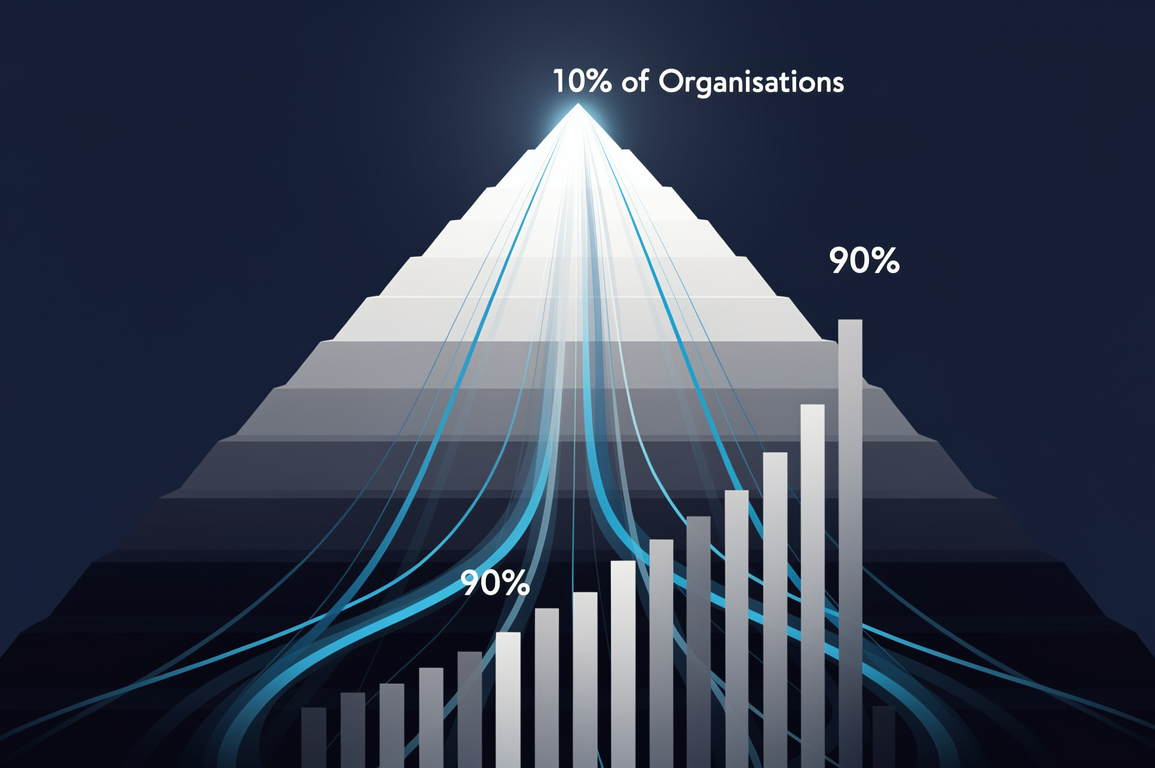

The professional services firm’s research reveals that approximately 10% of organisations—termed “AI leaders”—are capturing roughly 90% of the measurable returns from AI investments, creating what PwC characterises as a “winner-takes-most” dynamic that mirrors historical technology adoption patterns but at an accelerated pace.

The study, which surveyed 2,400 executives across 28 countries and analysed financial performance data from organisations with significant AI expenditure, identifies a critical inflection point in enterprise AI deployment. Whilst aggregate AI investment continues to climb—reaching an estimated $450 billion globally in 2025—the distribution of returns shows marked inequality.

“We’re observing a bifurcation that should concern boards and executive teams,” the report states. “The gap between leaders and laggards is not narrowing with maturity of the technology—it’s widening.”

PwC attributes this concentration to three primary factors: data infrastructure quality, organisational change management capabilities, and what the firm terms “AI-native” operating models that embed machine learning into core business processes rather than deploying it as isolated use cases.

The business impact manifests across multiple dimensions. Leading organisations report productivity gains of 25-40% in AI-augmented workflows, whilst the median organisation sees improvements of just 3-7%. Revenue growth attributable to AI-enabled products or services shows similar disparity, with top performers capturing new revenue streams whilst most organisations remain focused on cost reduction applications.

This divergence creates strategic implications for competitive positioning. Industries with high AI intensity—including financial services, technology, and pharmaceuticals—face the prospect of market consolidation as leaders leverage superior AI capabilities to capture market share. Organisations in the middle cohort face a critical decision point: whether to significantly increase investment to close the gap or risk permanent competitive disadvantage.

The talent dimension compounds these challenges. PwC’s data indicates that leading organisations have built multidisciplinary teams combining technical expertise with domain knowledge, whilst lagging organisations remain dependent on external vendors and consultants—a model that rarely generates sustainable competitive advantage.

The study also highlights a concerning pattern in capital allocation. Organisations achieving below-median returns continue to increase AI spending, suggesting that investment magnitude alone does not correlate with outcomes. This “throwing money at the problem” approach, PwC warns, risks creating stranded assets and executive disillusionment with AI’s potential.

Regional variations add complexity to the global picture. North American and Chinese organisations dominate the leader category, whilst European firms show stronger performance in regulated industries where governance frameworks provide competitive advantage. Emerging markets display the widest variance, with a handful of digital-native firms achieving leader status whilst traditional enterprises lag significantly.

The findings arrive as boards face mounting pressure to demonstrate AI returns. According to Daily Business Magazine’s analysis of the PwC data, organisations in the bottom quartile of AI performance face increased scrutiny from investors, with several high-profile cases of chief AI officers departing after failing to deliver promised results.

Looking ahead, PwC identifies several indicators that will determine whether this concentration persists or moderates. The maturation of AI tooling and platforms could democratise capabilities, whilst the emergence of specialised AI service providers might offer laggards a path to competitive parity. Conversely, leaders’ data advantages and organisational learning curves may prove insurmountable for late movers.

The study’s central message for business leaders is unambiguous: AI deployment is not a uniform rising tide lifting all boats. Without fundamental changes to data infrastructure, talent models, and organisational design, increased investment will likely yield diminishing returns whilst the performance gap continues to widen.